UPI powers India’s digital economy with billions of monthly transactions, but as adoption grows, so do fraud risks. This project explores how fraud prevention can shift from post-transaction detection to pre-transaction decision support.

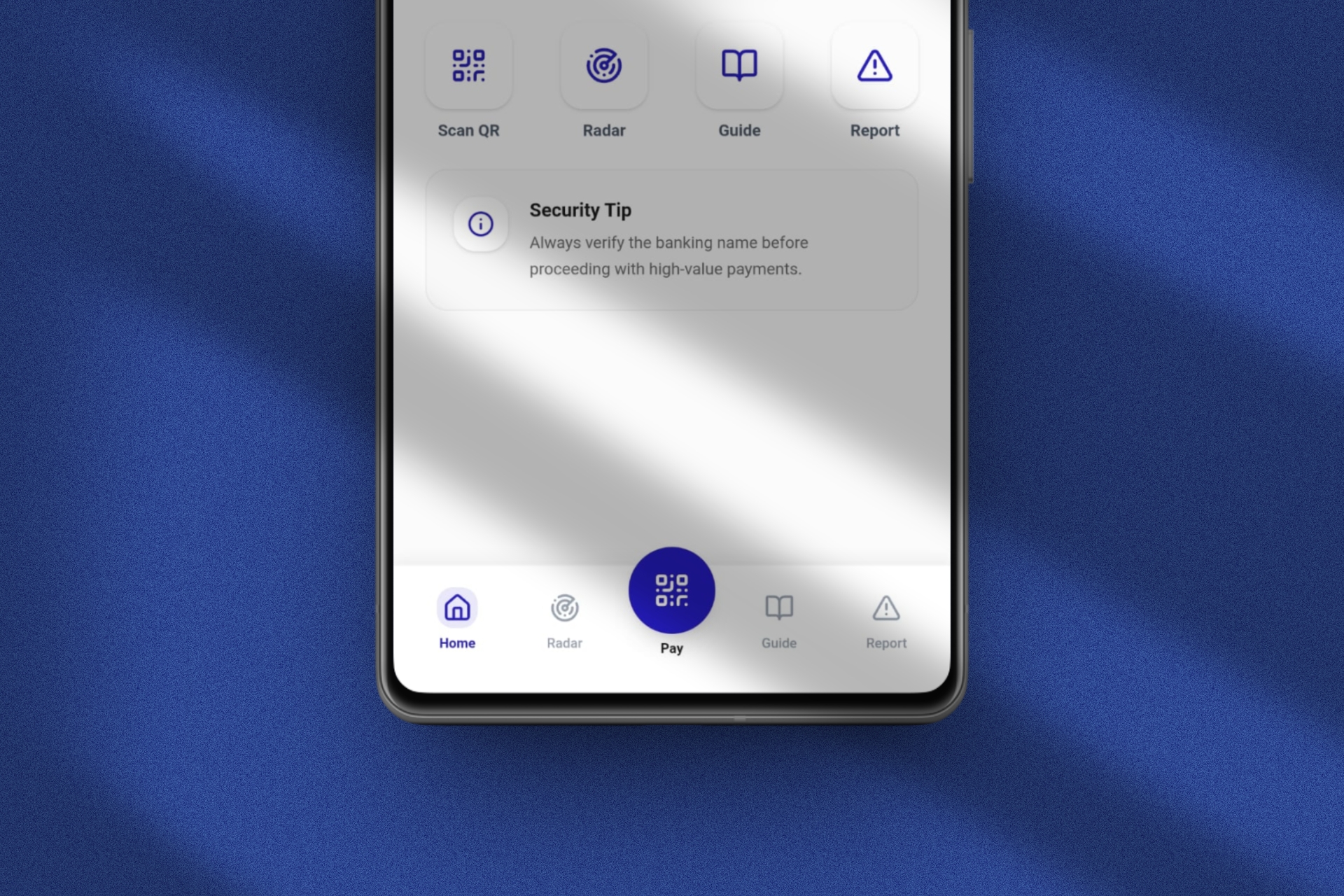

UPI Shield is a concept feature that introduces a real-time risk awareness layer within the payment flow, enabling users to make safer decisions before sending money.

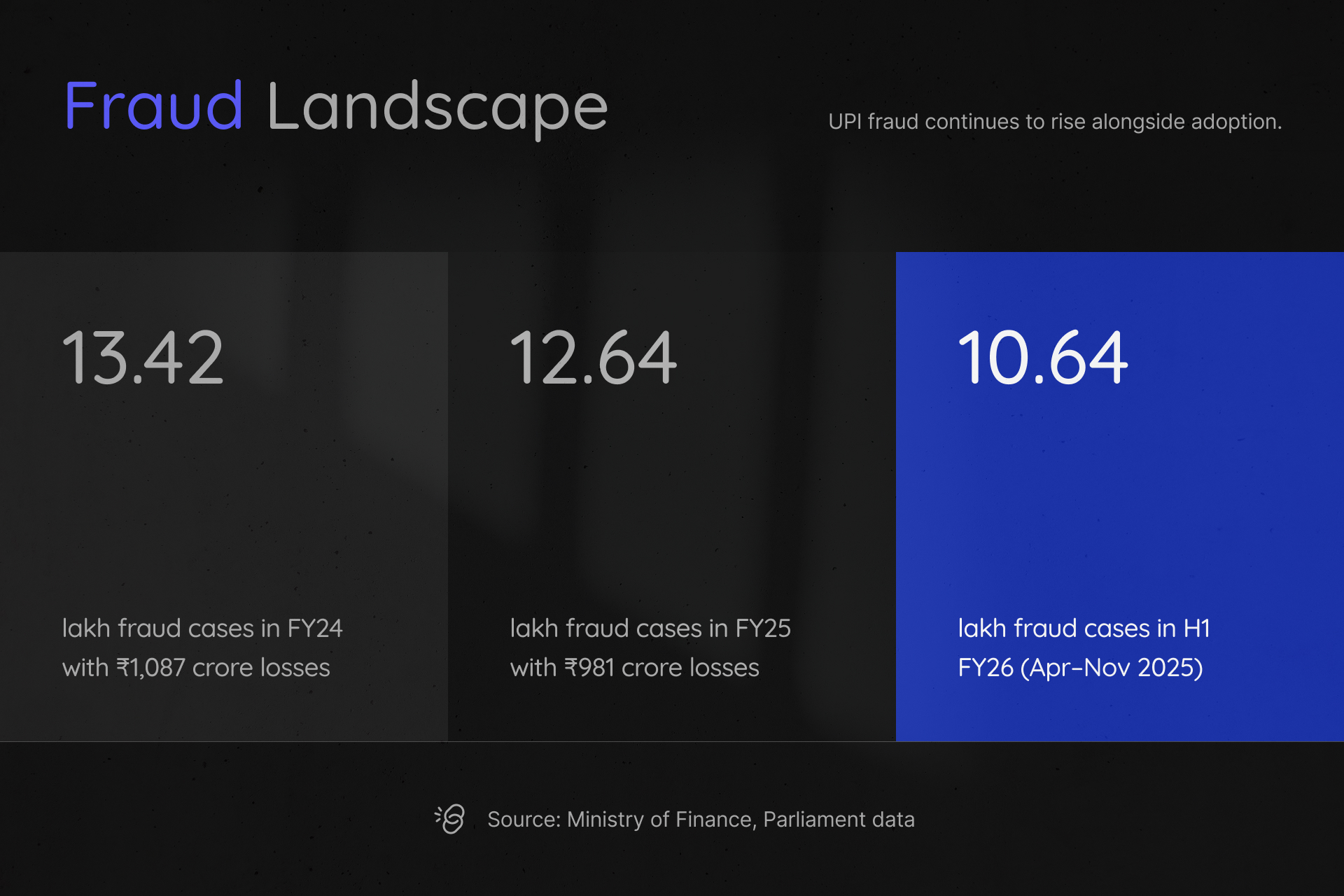

UPI is one of the largest real-time payment systems globally, with 400M+ users and 20B+ monthly transactions

However, fraud is scaling alongside adoption:

Most fraud does not occur due to system vulnerabilities, but because users are not equipped with the right signals at the moment of decision-making.

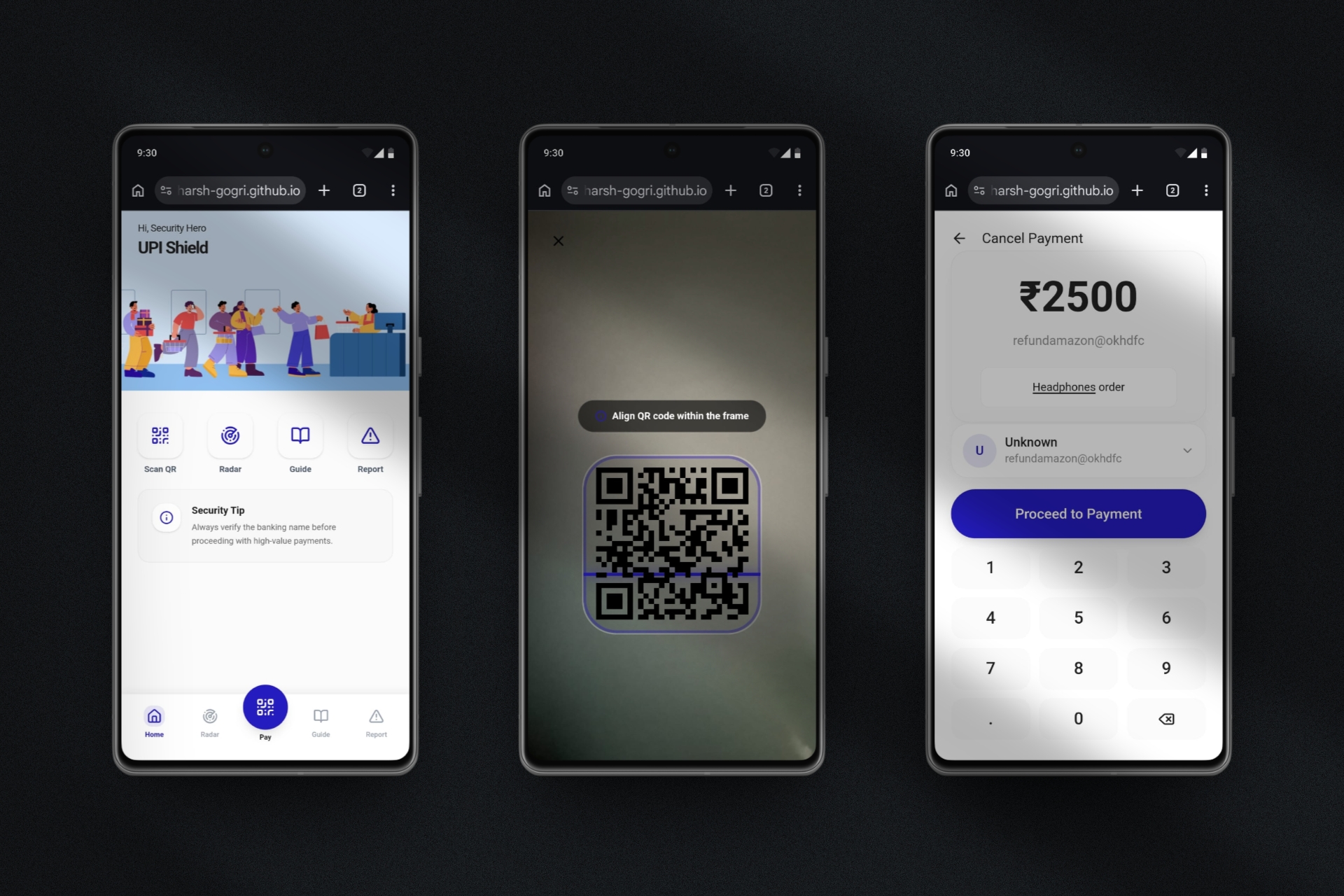

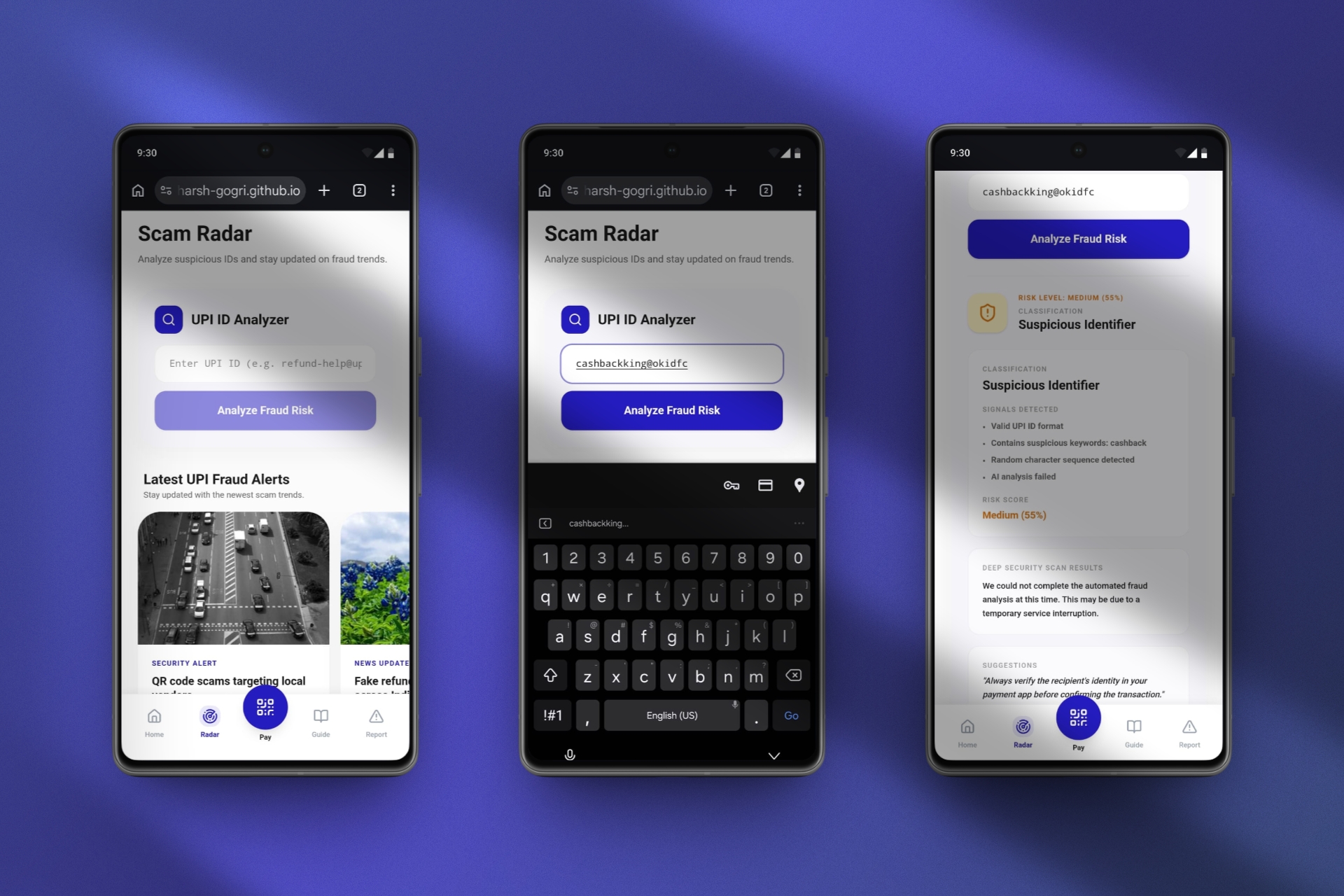

Today, users are expected to trust unfamiliar QR codes or UPI IDs without any contextual verification.

UPI fraud is a decision-stage problem, not a technology failure

There are two primary behavioral patterns observed:

Despite their differences, both groups lack real-time confidence signals during payments.

The opportunity lies in embedding lightweight risk awareness directly within the payment journey, without disrupting the speed that makes UPI successful. Instead of blocking transactions, the strategy focuses on:

Enable at least 30% of payment attempts to include a risk review within 4 months

UPI Shield introduces a lightweight, optional security layer integrated directly into the payment flow.

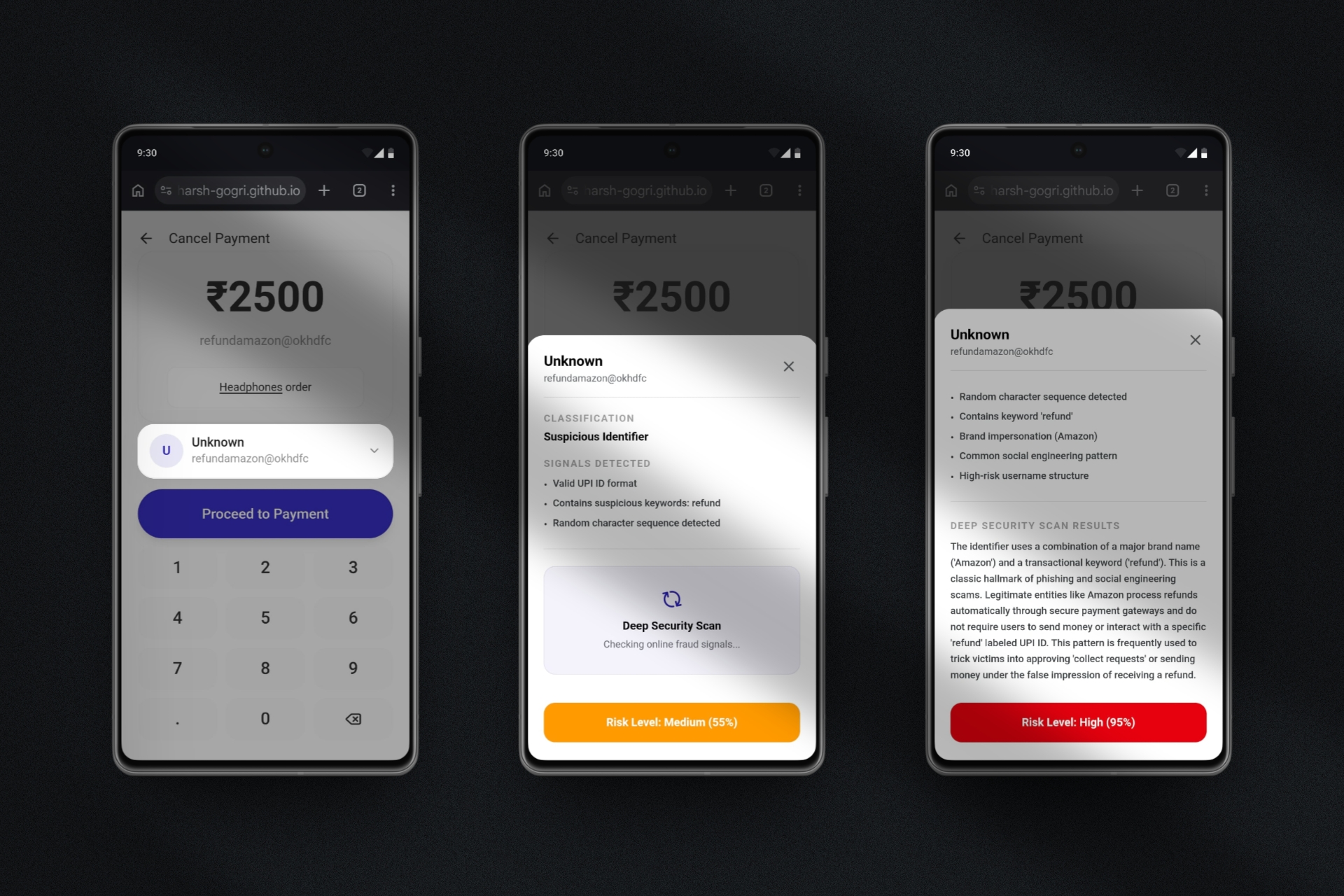

The risk scoring system is conceptualized as a multi-signal evaluation engine:

Balancing safety within a high-speed payment ecosystem required careful trade-offs across product, UX, and system design.

UPI’s core value lies in instant transactions. Introducing friction risks drop-offs and reduced adoption.

Decision:

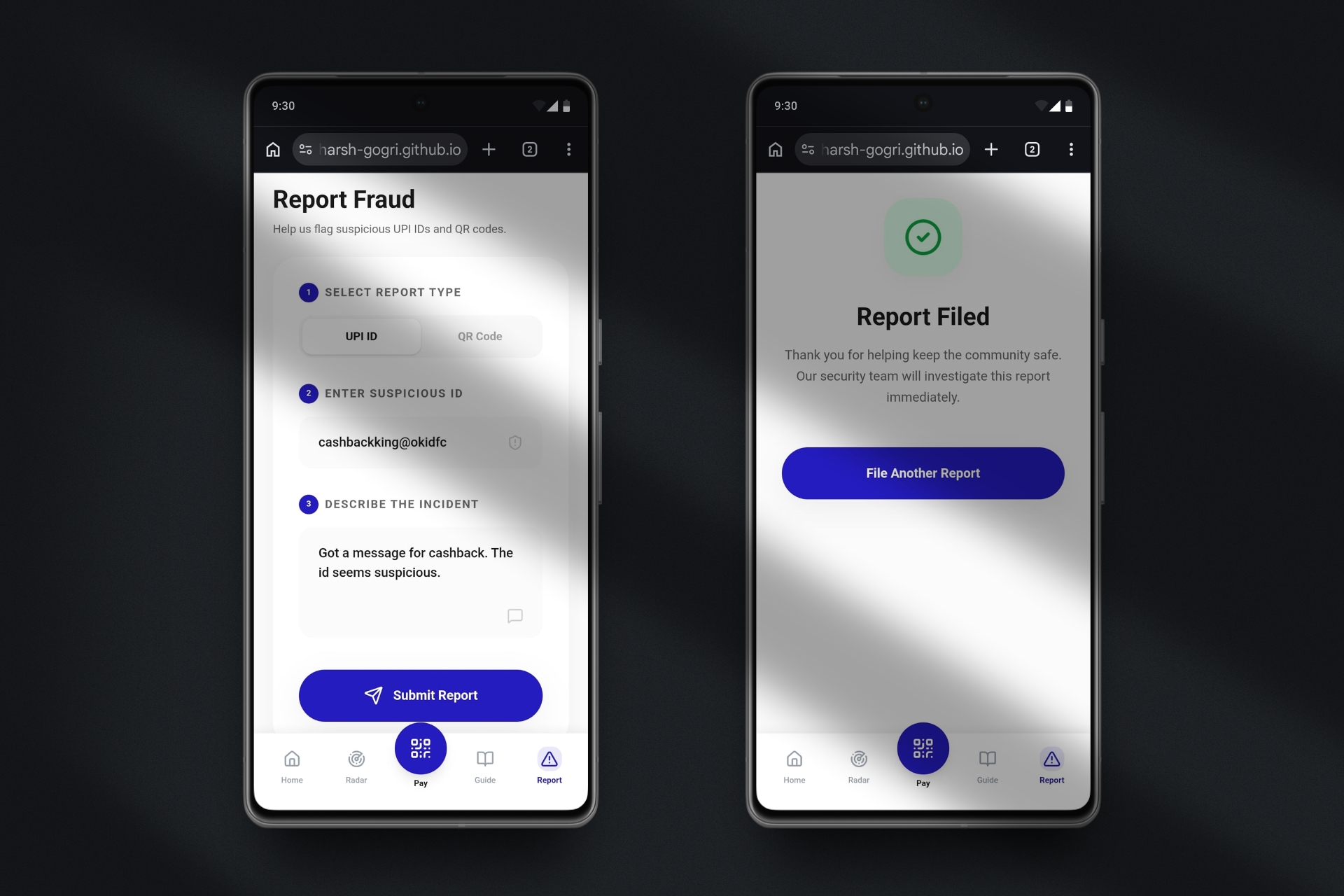

Keep all risk interactions optional and non-blocking.

Overly aggressive warnings can create alert fatigue, while weak signals fail to prevent fraud.

Approach:

Prioritize explainability — show why something is risky instead of relying on black-box scoring.

The project relied entirely on secondary research without user interviews or usability validation.

Approach:

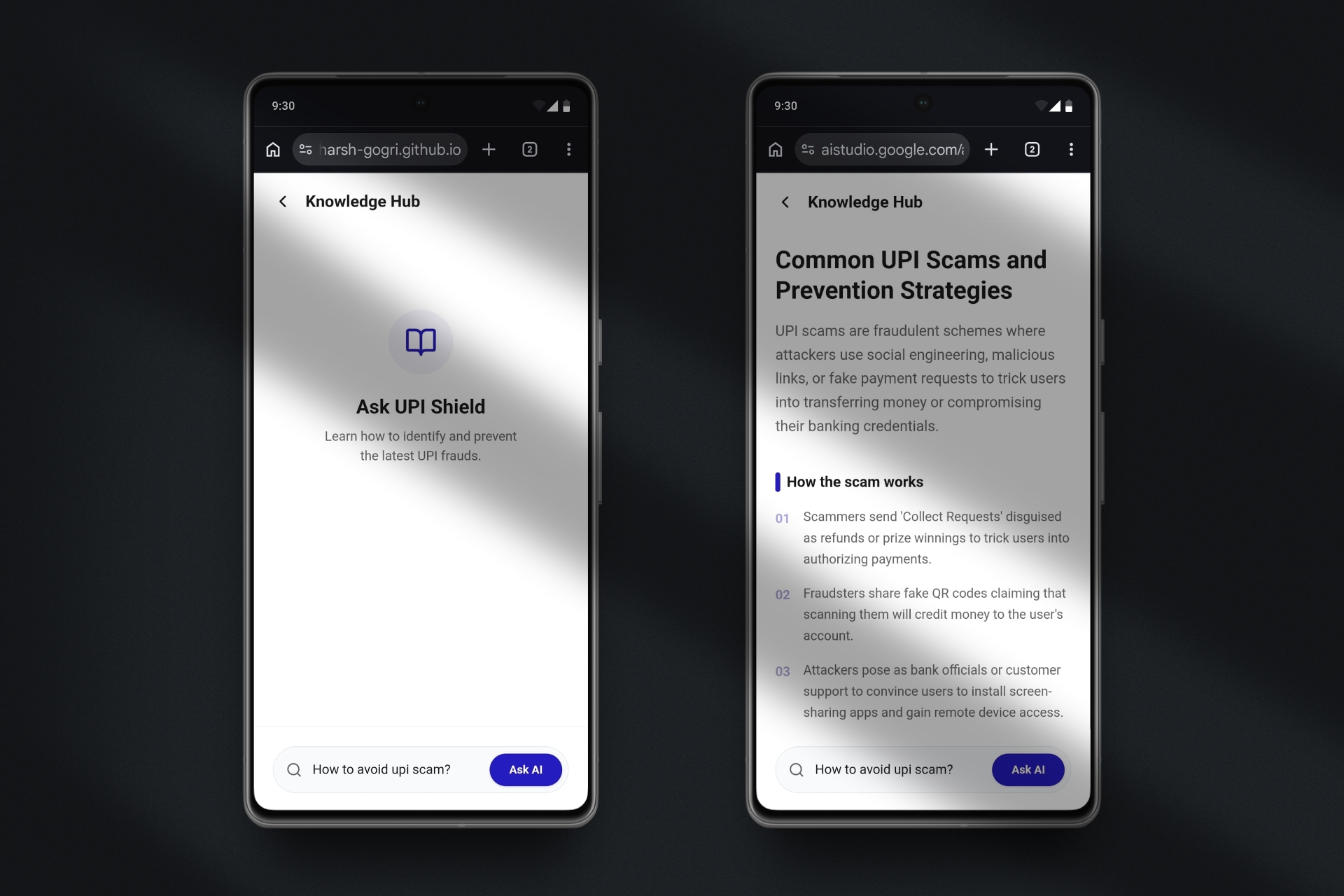

Ground decisions in industry data and known behavioral fraud patterns.

Implementation depends on multiple external systems:

UPI Shield is designed to influence user behavior at the most critical moment — just before a payment is completed.

By introducing contextual risk signals, the product aims to:

From a product perspective, this translates to lower fraud success rates and stronger trust in digital payments.

The primary success benchmark is achieving 30%+ engagement with risk signals before payment completion

.jpeg)